Tax Filing season in Thailand is going to start soon. Are you a foreigner in Thailand and want to get updates about the current tax rates and regulations? Then this article is for you to educate you on the recent policies of paying tax in Thailand for foreigners for the 2022-23 season tax filing.

Thailand is a prevalent location for retirees and ex-pats from all over the world. It’s important to understand what types of income are subject to taxation under Thai law.

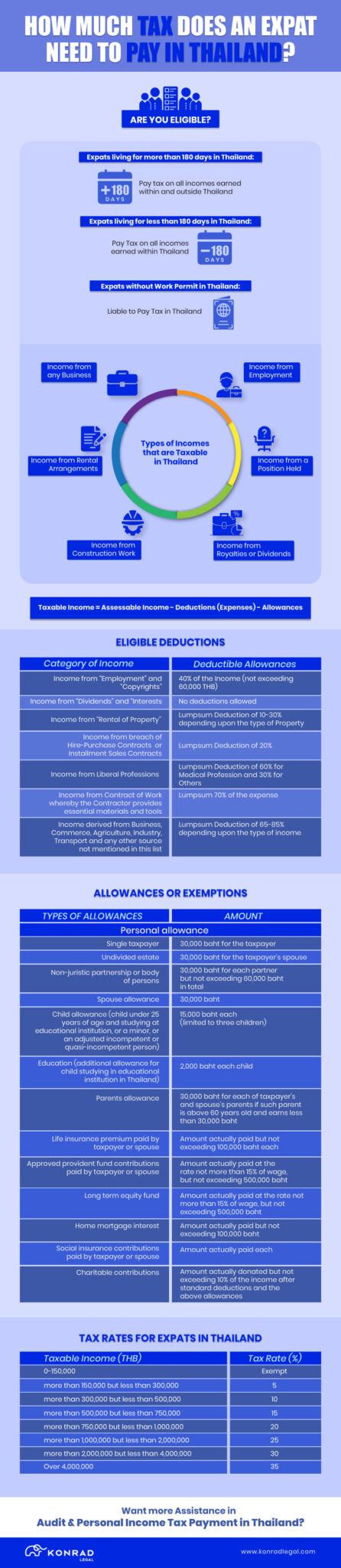

Personal Income Tax in Thailand 2022-23

Thailand applies the source rule and residence rule to its Personal Income Tax (“PIT”). Generally, regardless of the source of generation of income, PIT is applicable for all.

Whether you receive a payment in Thailand or abroad, the source rule still applies to foreigners. It is applicable for all who receive Thai-sourced income and are therefore subject to PIT in Thailand.

Depending on the tax residency status of a foreigner, the residence rule is applicable to their foreign income. Note that, a tax resident is a foreigner spending a minimum of 180 days in Thailand during any tax year. The Thai tax year corresponds to the calendar year. If a tax resident brings foreign income into Thailand during the same tax year, it will be subject to PIT. However, PIT in Thailand does not apply to income from foreign sources if the foreigner is not a tax resident.

Progressive PIT tax rates range from 0-35% of the net assessable income after subtracting exempt incomes, costs, and allowances. Generally, taxpayers must submit the yearly PIT return by March 31 of the subsequent (tax) year (PND 90 or 91). This is applicable to foreign citizens receiving specific types of income. Rental income or company revenue is such a type of income. For this, the foreigner must submit a half-year PIT return (PND 94) by September 30 of the same tax year.

Foreign nationals falling in the eligibility bracket for PIT must apply for a tax ID number. This application must be within 60 days of the date they start making taxable income.

Gift Tax in Thailand 2022-23

One specific sort of PIT for which the aforementioned source rule and/or residence rule also apply is the gift tax. Foreigners receiving any moveable property (cash, a car, jewelry, etc.) as a gift or stipend must pay a gift tax. The applicable rate is 5% of the amount exceeding 20 million THB in each tax year. Additionally, this is applicable in all cases of assistance from an ancestor, a descendant, or a spouse.

The 5% Gift Tax shall, however, is applicable to the share over 10 million THB in each tax year. This is mandatory in cases of transfer of ownership of the moveable property to a foreigner. Processes pertaining to such transfers can be a formal ceremony or on customary occasions. Additionally, it can be due to moral obligation by a person who is not a descendant, or a spouse.

Last but not least, the 5% Gift Tax is applicable on the appraised value of immovable property. Land, buildings, condominium units, etc. are examples of such properties. This is applicable if the value exceeds 20 million THB per legitimate child in each tax year. It is also applicable if there is an ownership transfer from Parents to their legitimate children, but not adopted children.

Withholding Tax or WHT in Thailand 2022-23

Withholding Tax (or “WHT”) shall apply to certain categories of income. Additionally, in all types of transactions, there is a greater obligation to deduct WHT from both tax residents and non-tax residents. The following table will present you with the idea of categorization of WHT for tax and non-tax residents of Thailand:

With a Double Taxation Agreement (“DTA”) in effect between Thailand and the nation where the foreigner is a tax resident, or when other domestic laws, such as the Investment Promotion Act, are applicable, there is a reduction or exemption in the WHT rate.

Value-Added Tax or VAT in Thailand 2022-23

Before beginning commercial operations or within 30 days of earnings reaching the level of assessable income, any foreigner who regularly sells goods or renders services in Thailand and whose annual revenues exceed 1.8 million THB must register for Value Added Tax (“VAT”).

For your information, foreigners who offer an electronic service (or “e-Service”) from outside to Thai users who have not registered for VAT must also do so.

However, some activities—such as those covered by an employment contract, the renting of real estate, and acting/actress performances—are free from the VAT.

The standard VAT rate is 7% of the value of the goods or services. Activities like exporting goods and services are exempt from paying VAT. Additionally, eligible payers must file monthly VAT returns (P.P. 30 or P.P. 30.9) by the 15th day of the following month.

No matter if they have registered for VAT or not, importers in Thailand are likewise liable to VAT. In this case, at the time of customs clearance for imports, the Customs Department collects the VAT.

Specific Business Tax or SBT in Thailand 2022-23

Any foreigner who sells or transfers an immovable property within five years of the date of acquisition must pay a Specific Business Tax (“SBT”) at a rate of 3.3% (including a 10% local tax). Note that, this tax is payable at the time of the transfer at the Land Office. However, the tax rate depends on the greater value, i.e., either the appraised value or the sale price.

Stamp Duty in Thailand 2022-23

Depending on the circumstance, taxpayers must apply for and pay Stamp Duty (“SD”) in cash at the Revenue Office. Alternatively, they can also do so through the e-stamp duty system on the website of the Thai Revenue Department for the execution of specific instruments. These documents include leases for land or buildings, the sale of shares, the transfer of real estate, the hiring of labor, the borrowing of funds, powers of attorney, guarantees, and the duplication of documents.

Depending on the transaction, the SD rate may be fixed or computed as a percentage of a specified value. For illustration:

- rental of land or building is subject to an SD of 0.1% of the rental fee, or key money, or both, for the entire lease period;

- transfer of share is subject to an SD of 0.1% of the paid-up value of the shares or shares sale value, whichever is greater;

- transfer of immovable property is subject to an SD of 0.5% of the appraised value or sale value, whichever is the greater

- hire of work contracts are subject to an SD of 0.1% of the remuneration provided for the work under the contract

- duplication of an instrument is subject to an SD of 1.00 THB if the SD of the original instrument does not exceed 5.00 THB, or 5.00 THB if the SD of the original instrument exceeds 5.00 THB.

The lessor, share transferor, contractor, lender, a seller of the land or building, guarantor, etc. in the transaction is responsible for paying or attaching the SD. A beneficiary or the holder of any of these legal documents may have to pay SD to implement the document.

Inheritance Tax in Thailand for Foreigners in 2022-23

If the net inheritance value from each testator exceeds 100 million THB, any foreigner who is domiciled in Thailand under the Immigration Law is required to pay inheritance tax within 150 days of that date, together with the tax payment. If the recipient is an ancestor or a descendant of the testator, a rate of 5% is applicable. Note that, this is applicable to the portion of each testator’s net inheritance value that exceeds 100 million Thai Baht. However, this is applicable to the amount after subtracting any liabilities. Additionally, when the net inheritance value exceeds 100 million THB, a rate of 10% is applied.

For your information, foreigners will also be subject to the aforementioned tax rates, but only if their inheritance is located, registered, withdrawn, or claimed in Thailand.

Land and Building Tax in Thailand 2022-23

A Land and Building Tax (also known as the “L&B Tax”) must be paid by any foreigner who owns the land, a building, or a condominium unit in Thailand by the end of April each year.

Depending on the use of the land and/or building, such as agricultural, residential, unused/vacant, or other purposes, the L&B Tax is now determined based on progressive rates ranging from 0.01% to 0.70% of the net appraised value of the land, building, and/or condominium unit.

What We Can Do for You?

When it comes to Accounting, Audit, and Taxation in Thailand, we cater to a wide spectrum of related services for foreigners in Thailand. They are as follows:

Accounting Service:

You will certainly need an accountant or reliable Accounting Services in Thailand to get all your calculations right and save taxes. To track your profits and pay taxes timely, talk to us today!

Annual Account Audit

We take pride to conduct successful audits of all types. Be it planned and requested audits or Internal and external audit coordination we manage ALL these effectively and diligently.

Half-Yearly Account Audit

Get a simplified forecast and a summary of your actual business performance. To get your Half-Yearly Audit Report on time in compliance with Thai Accounting Standards, Consult Us!

Tax Audit Service

We can identify the weaknesses in the accounting system and ensure real financial benefits for your business to facilitate its smooth continuity. Therefore, for all support on tax in Thailand for foreigners, book your Free Consultation Session!

Bookkeeping Service

We can record transactions, compare computer reports, cater to tax obligations, review invoices, and statements, and all activities to provide complete Bookkeeping Services in Thailand.

Open a Corporate Bank Account

Are you eligible to open a bank account in Thailand? If you are Thai, it is possible! However, for Foreigners in Thailand, we make it possible. Therefore, to get your Corporate Bank Account in Thailand, Contact Us!

Notary Service

Do you need to authenticate your signature or any document in Thailand? Our Authorized Notarial Service Attorneys specialize in all 7 forms of Notary in Thailand for all documents. Drop in with your requirement!

Tax Refund Application

Did you miss filing a tax refund for the previous year? Do not repeat the same. Therefore, let us help you in the process so that you can file your return on the right date. Trust Us, we do the follow-up! Consult Us!

Corporate Income Tax

For juristic companies in Thailand of any form under Thai or International Accounting Standards, we hold a reputation as the leading Taxation Firm in Thailand. We cater to all necessary requirements in paying taxes in Thailand for foreigners. Get in touch with us!

Payroll Management

You tell us the task, and we can manage all related to your employee paychecks, pension funds, or filing employer’s returns, we will do the complete Payroll Management for your company in Thailand.

So, if you are looking for any or all of the above-said services, please feel free to book your free round of consultations today. Email us your requirement at officer@konradlegal.com to grant us the opportunity to facilitate the payment of tax in Thailand for foreigners.

{kind=link}