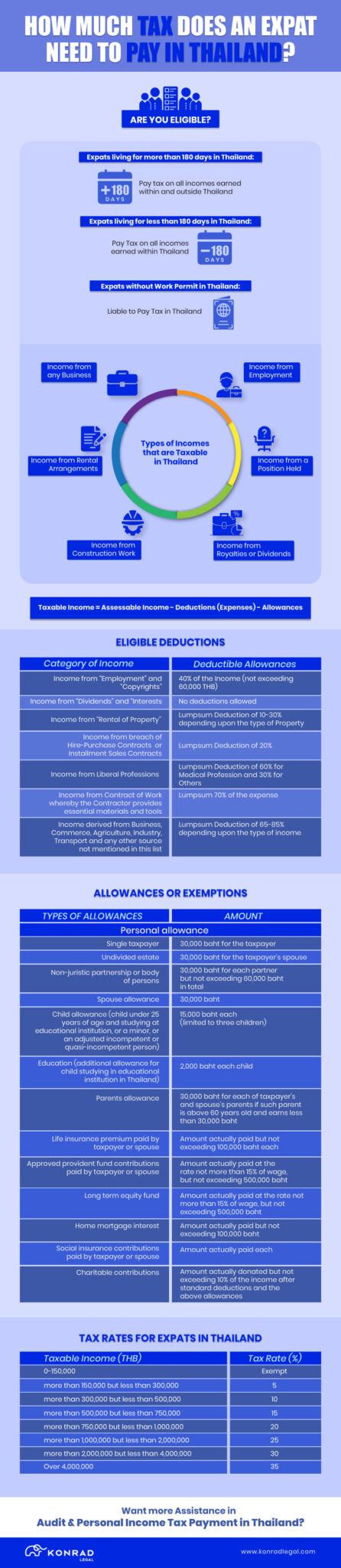

As a foreign investor or company in Thailand, it is essential for you to know about the income tax obligations in the kingdom. We all know that the Royal Thai government offers various tax and non-tax incentives to foreign investors. Therefore, unless you do your tax planning, you will never be able to assess whether you are eligible for the tax benefits or not. This article will serve as your comprehensive guide by highlighting all you must know about Income Tax for Foreign Business in Thailand.

Overview

The tax obligations on foreign business in Thailand depend significantly on the type of business it is doing here in the kingdom. The reason behind this is the following:

- There are certain Board of Investment tax incentives that are applicable only to eligible businesses and activities. Check out the list of activities eligible for tax incentives under BOI Thailand. Therefore, if your business falls on this list, you may release yourself from various types of bills and taxes.

- If you are into manufacturing business, then there are certain tax benefits from the Industrial Estate Authority of Thailand. Although you have to satisfy certain conditions, yet, on qualifying you can enjoy VAT exemptions and export-import tax exemptions. Check out the eligibility and tax benefits under IEAT Thailand.

- There are double tax treaties between Thailand and 61 countries. These tax treaties remove the mandates of paying tax to foreign companies for the same income in both Thailand and the native nation. Therefore, it is always wise to check whether you are liable to pay double tax or not. These privileges of tax deduction also sometimes depend on the type of business you are planning to do in Thailand.

Note that, to ascertain the tax liability of your business in Thailand, you must check through the above three points. It might be somewhat tricky for you to review and consider all the aspects associated with the same. Therefore, you must go on consultation with a professional Thai tax law firm to clear your mind on this.

Types of Income Tax for Foreign Business in Thailand

Foreign companies operating in Thailand may be subject to various types of taxes. Here are some of the main taxes that foreign companies may be required to pay in Thailand:

Corporate Income Tax (CIT)

Foreign companies that generate income in Thailand are generally subject to CIT at a standard rate of 20%. However, specific tax incentives may apply based on the type of business and industry. Check out the Corporate Income Tax rates of Thailand below:

Value Added Tax (VAT)

VAT is applicable to the sale of goods and services in Thailand. The standard rate is 7%, but certain goods and services may be subject to a reduced rate or exemption. However, the general rate of VAT applicable to various products and services in Thailand is as follows:

Withholding Tax

Foreign companies making payments to individuals or other entities in Thailand may be required to withhold tax on certain types of income, such as interest, dividends, royalties, and payments for services. The withholding tax rates vary depending on the payment type and the recipient’s tax status. Following are the updated rates of withholding Tax in Thailand:

Specific Business Tax (SBT)

Certain types of businesses, such as financial institutions, may be subject to SBT in addition to CIT. SBT rates vary depending on the type of business.

Property Tax

If a foreign company owns property in Thailand, it may be subject to property taxes. These taxes can include land and building taxes. Check out here to know all about Property Tax Regulations and Rates in Thailand.

Stamp Duty

Stamp duty may apply to various documents, contracts, and transactions, such as property transfers and certain legal agreements.

Excise Tax and Custom Duties

Certain products, such as alcohol, tobacco, and petroleum, may be subject to excise tax. Foreign companies involved in producing or importing such products may need to pay excise tax.

Moreover, if a foreign company engages in international trade with Thailand, customs duties may apply to the import and export of goods.

Transfer Pricing Regulations

Thailand has transfer pricing regulations to ensure that transactions between related entities are conducted at arm’s length prices for tax purposes. Foreign companies must comply with these regulations when dealing with Thai affiliates. Go through our article to learn more about transfer pricing in Thailand.

Income Tax Payment Deadlines for Foreign Business in Thailand

In Thailand, tax deadlines can vary depending on the type of tax and the taxpayer’s circumstances. Here are some general guidelines for tax payment deadlines in Thailand:

The Bottomline

This article has covered a majority of the nooks and corners of income tax applicable to foreign businesses or companies in Thailand. We hope that it will help you in your understanding of the tax regime of Thailand for your business.

However, it is always wise to have a professional Thai tax consultant by your side. In addition to tax payments, we also specialize in helping Thai and foreign businesses with bookkeeping, accounting, and payroll management support. To get all the services under one roof, email us at officer@konradlegal.com for expert support.

{kind=link}